Before you retire or leave full-time employment for other pursuits, consider the impacts of your decision on the financial well being of your future. The transition to your next phase of life, whether full or semi-retirement, adventure seeking, or family driven, requires thoughtful planning to avoid needless surprises that can mean the difference between financial success or financial stress. Whether you have been planning your retirement for decades or days, contemplating these six key retirement elements can help you avoid unexpected problems.

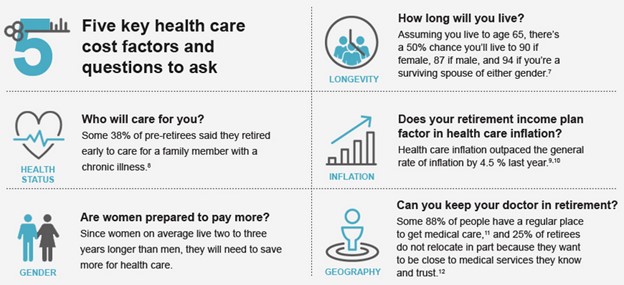

Health insurance and the cost of health care throughout your retirement years is the first key consideration. If you have been on an employer-sponsored plan, it is crucial to understand the depth and breadth of coverage options and associated costs when you leave your full-time employment. Health care costs will rise as you get older, and according to Fidelity Investments, the average 65-year-old couple will spend $280,000 on health care costs during retirement.

Fidelity Investments Retirement Planning

Medicare is a definite help once you reach the age of 65; however, it does not cover the cost of everything, which is why supplemental health insurance becomes necessary. Learn what Medicare does cover and then explore insurances that will fill in the gaps you most need to cover, such as dental, vision, and long-term care. If you are younger than 65, you will have to supply your health care coverage through vehicles like COBRA if that is an option available through your current employer. If not a COBRA plan you can try the Affordable Care Act (Obamacare). Employing this option and depending on your income, you may even qualify for a subsidy, but open enrollment periods are limited, and you must plan your retirement accordingly. Other insurance options include less robust coverage choices with short-term plans. These plans are only viable for generally healthy people who have no pre-existing conditions.

You may think you want to retire fully; however, it is not uncommon to shift gears and decide for a sense of purpose that you want to work part-time in your “retirement”. Depending on your age, part-time work may affect your social security benefits if you have already begun claiming them. The second key consideration then is to know what your social security strategy is. Most retirees do not want to hold off on receiving their benefits at the age of 62 but the longer you can delay the larger your monthly checks will become. Your benefit increases 6 percent annually until full retirement age and then 8 percent annually until you reach the age of 70.

Since over half of Americans ages 60 – 64 are still working full or part-time, it is critical to know what effect your wages will have on your social security benefits. Nearly one-third of Americans ages 65 – 69 are still in the workforce, and their earned wages are also affecting their social security benefits. The penalty, when exceeding the earnings cap, is short-term substantial. If you make more than $17,640 in 2019, for every dollar you exceed the cap, your benefit will be reduced by one dollar for every two dollars you earn. The monetary penalization will come back to you when you reach full retirement age in a higher monthly benefit check however it depends on your overall income, and up to 85 percent of your benefit is subject to federal income tax. The scenarios get complicated, and it is essential to understand the nuances of social security benefit rules and how they relate to your situation.

When you are preparing to retire the third key consideration is evaluating your tax strategies based on your income. You may have provided for passive and multiple streams of income, and they have distinct tax implications depending on the type of financial retirement vehicle or product. Many people have a variety of retirement incomes such as 401(k)s, IRAs, taxable savings, investment accounts, health savings accounts (HAS) and business or trust incomes. All of these assets have optimal times to tap into for retirement income because of tax consequences. Know your strategy especially since your annual income can affect what you pay for Medicare.

The fourth key consideration is to check what the risks are in your retirement accounts and income plans. By the time you retire, most of your financial portfolio should be in risk-averse financial vehicles. Evaluating and allocating your portfolio to include financially stable products like bonds or well-researched annuities is essential. If you do not have to be overly risky in your strategy, then, by all means, do not be. It is better to live comfortably, or even modestly, in your retirement years then throw everything you have on a betting wheel and come up empty-handed. If you have had the same investment strategy since you were in your early twenties, it is beyond time to re-evaluate your choices.

The fifth key consideration is to prepare for an adverse event by having a financial cushion. Most financial advisors recommend that you keep several years of your income away from market-driven investments and maintain the cash in more stable vehicles like money markets, cash, and other investments that have minimal risk. The rule of thumb is never put the money you need to maintain your lifestyle for the next three years at risk. That allows you time to respond to any adverse event that may crop up while maintaining your retirement lifestyle. This way, if the investment markets are down, you will not have to sell those assets, potentially at a loss, to survive.

Finally, the sixth key consideration is to prepare emotionally for the ups and downs and loss of identity that you have cultivated during your career. Many retirees have a difficult time transitioning to retirement when so much of their life has been defined by what they did for a living rather than who they are as a person. Many people become inextricably linked to their identity through their career and moving into retirement without that career identity can create unforeseen depression. If you do not have to work, it is important to create a new life purpose. Volunteering and mentoring is a fantastic way to help your fellow humankind and ward off feelings of loneliness and lack of self-worth. Also, prepare yourself that the money and those asset accounts you have worked so hard for all your life are going to reflect the change of retirement brings. It can be hard to watch withdrawals for your retirement living chunk away at what you worked so hard to build. Do not go to places of dark imaginings. Retirement spending is exactly what you worked for your entire life.

It isn’t always easy to transition to retirement life. Your working norm must be redeveloped into your retirement norm. Think carefully through the issues that will be most important to your success and well being BEFORE you retire. Contact our office today and schedule an appointment to discuss how we can help you with your planning.

— By Rebecca W. Geyer, Founder of Geyer Legal Group, PC